The U.S. healthcare sector is one of the country’s major economic pillars and it has become an industry that is now too big to fail. This massive, interconnected ecosystem – spanning insurance, pharmacy services, and administrative clearinghouses – supports millions of American jobs and underwrites economic activity across the country. A deep reliance on healthcare as an employment lifeline is precisely why meaningful reform faces such significant challenges. Changes that seek to reduce cost of care or nudge the industry towards a free-market pricing structure collide with entrenched establishment interests.

While this stalemate has persisted for decades, the pernicious and formidable growth of the healthcare administrative state has now made meaningful change politically impossible. With healthcare costs surging and resources increasingly scarce, the system desperately requires the equivalent of a GLP-1 agonist to shed its considerable administrative weight. Without such an intervention, healthcare delivery may soon become so ineffective that it struggles to provide value or care to anyone.

A Pulse on the Matter

In 2023, the healthcare industry directly employed over 17 million people1, accounting for 9.3% of total employment or about 1 in 6 private sector jobs. Within most healthcare systems, approximately 40%2 of employees aren’t involved in direct patient care. Workers in this category typically fill roles such as managers, coders and billers, computer and equipment technicians, administrative assistants, and community resource coordinators. These roles are found in nearly every brick-and-mortar health organization in the United States, making their redundancy costly.

At 770 administrative workers per $1 billion of revenue3, healthcare employs nearly eight times the number of administrators found in other sectors (100 workers per $1 billion). Administrative costs have accounted for 15–30%4 of total national health expenditures over the past three decades, far exceeding other high-income countries. These costs do not reflect supporting employment in adjacent industries. While cumulative figures are challenging to calculate, conservative estimates suggest that administrative costs have added $10–20 trillion5 to U.S. healthcare spending since the mid-1990s. Despite total annual spending soaring from $1 trillion in 1995 to $4.9 trillion6 in 2023, attempts to increase efficiency through M&A-driven synergies across health systems consistently fail to deliver value.

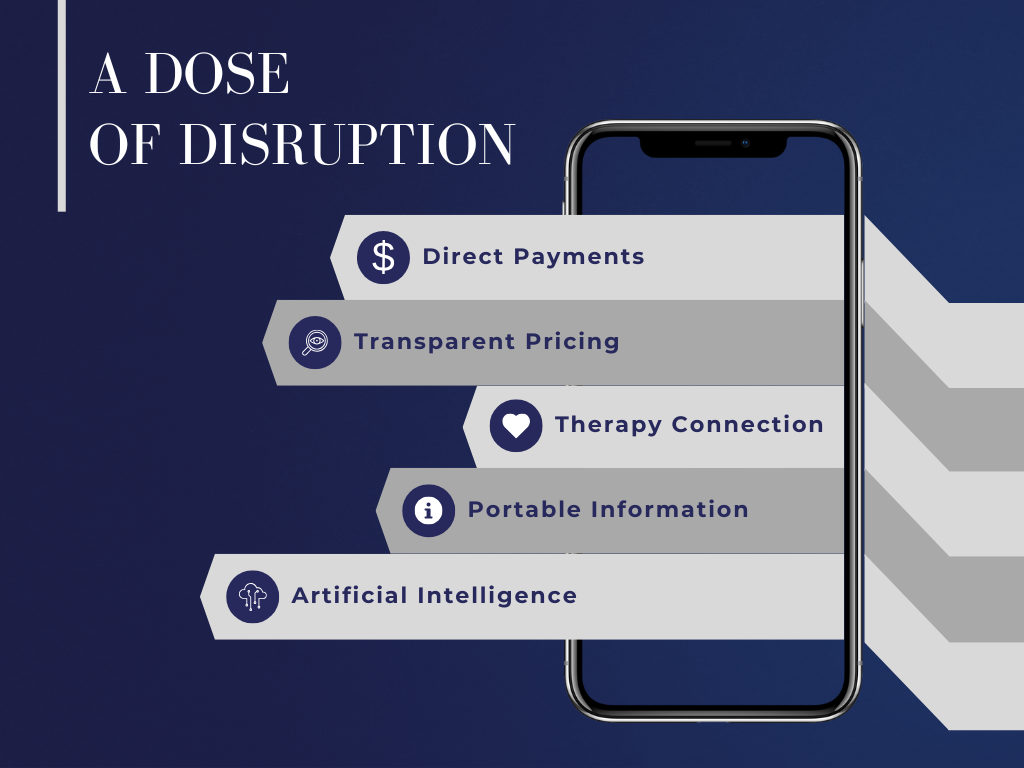

Five Principles for Disruption

The industry is undergoing early but significant disruption. A wave of new and innovative startups is empowering patients to interact with the system more directly. New companies are introducing payment and accessibility models that streamline administrative processes long associated with traditional healthcare delivery. We believe five overarching design principles can guide these necessary changes. The critical caveat is that their successful implementation will result in significant reductions in healthcare employment and will be met with fierce, organized resistance.

Direct Payments

The primary principle centers on enabling direct payment between patients and providers. By facilitating models such as direct primary care or allowing for the direct payment for individual services, patient-consumers can bypass the bureaucracy associated with insurance billing and third-party payers. This would be effective for healthy individuals, who can manage most routine health needs with episodic visits. Direct payment models foster a more transparent relationship between patients and providers, improving satisfaction and outcomes. Concierge care and subscription services are examples of these arrangements, but providers participating in traditional care models can create separate cash rates for individual services. These rates can feature additional discounts if services are paid in full on the same day.

Transparent Pricing

The most market-oriented disruption would be the establishment of transparent service pricing. The transition to deductible health plans exposed patients to higher out-of-pocket costs but left little ability to shop and compare with similar services. Current regulations enable service prices to be set through confidential negotiations between insurers and providers, which inhibits the creation of a true healthcare marketplace. There often are significant differences in prices for many common tests including X-rays, ultrasounds, and MRIs. The fix could include pricing information featured on a mobile application that displays the cash price of a service compared with average insurance cost for similar services across healthcare facilities. When patients can easily compare services across healthcare systems, they are empowered to make more informed choices. Transparent pricing encourages provider competition, lowers costs, and reduces overhead by eliminating complex processes associated with traditional medical billing.

Therapy Connection

Soaring prescription drug costs have been the single biggest obstacle preventing patients from connecting with and maintaining needed treatment. An all-too-common scenario is that a patient tries to pick up a medication only to be confronted with a material price increase or that the drug is no longer covered. Much of the responsibility lies with Pharmacy Benefits Managers (PBMs). These middlemen and procurement specialists have evolved from third-party players negotiating drug discounts to becoming one of the major drivers of prescription costs. Originally, these intermediaries helped secure savings for insurers and patients, but industry consolidation – especially after the Affordable Care Act of 2010 – evolved the business model into a profit lever for insurance companies.

Today, PBMs and similar entities impose significant markups on essential medications, increasing costs for patients and manufacturers. To address this, disruption is needed to bypass the middleman and eliminate preferred formularies. There are now several platforms that connect patients with needed prescription drugs and medical devices. Direct sourcing and distribution models can streamline supply chains, lower costs, and improve access to necessary treatments. Pharmacy startups are currently purchasing several popular drugs directly from pharmaceutical companies and adding a nominal markup. There is no rebate system or price manipulation in exchange for preferred formulary placement. Any drug that the pharmacy carries will display the list price plus the same small markup. In addition, many pharmaceutical companies are offering direct cash price options to patients for brand-name drugs not yet distributed through startup pharmacies.

Portable Information

Health data interfaces should deliver a seamless, integrated user experience for all industry stakeholders consistent with an Apple-like design philosophy. This reduces unnecessary service duplication and streamlines care coordination. The fundamental way health information is managed has largely remained unchanged; the previous paper-based processes were simply digitized. Nobody reimagined or reengineered how mobile patient data could be leveraged to improve care. Despite being roughly 15 years since the widespread use of electronic health records (EHRs), patient medical information remains proprietary to the health system from which one receives services. There have been incremental advances toward EHR interoperability, but true portability of patient records remains elusive.

The advent of wearables and external digital health information adds urgency to this issue, because there is now a substantial trove of health data generated at home that requires integration with health institutions. Several innovative startups are working on platforms for health record aggregation, secure transfer, and data interoperability. Supported by the Cures Act (2016) and using many technologies including blockchain, the ground is fertile for a winner to emerge.

Artificial Intelligence

Artificial Intelligence (AI) promises to deliver a dizzying portfolio of productivity gains, efficiency enhancements, and new competencies that will disrupt healthcare in several ways. Most important for patients are tools for diagnostic assistance, where various AI systems can enhance physicians’ ability to diagnose heart attacks, detect important findings on imaging, assist in surgeries, and analyze blood work. AI has been instrumental in improving the quality of virtual visits and the increasing sophistication of home “symptom checkers”. Patients can employ these tools to prevent unnecessary, time-consuming visits. For physicians, AI systems can help with medical record documentation, billing, and coding to increase accuracy, shorten documentation time, and maximize revenue. At a system level, AI can analyze the vast trove of health data to anticipate patient behavior, predict rising risk of disease, and optimize resources to meet future care needs.

Taken together, these five principles provide a framework for a simpler, more direct, and patient-centered healthcare system – one that leverages technology and innovation to deliver better outcomes. The true disruption comes from shattering the agency concept of the “system’s patient” and the “insurance company’s member”. Uncoupling that nexus will directly dislocate the service redundancy currently supporting the employment status quo. This, undeniably, is the single most significant hurdle to achieving true healthcare reform.

Many similar ideas have been proposed within the current delivery system, and each time the same factions arise to nip them in the bud. But if external disruptors can drive change, they can lay the foundation for a market-based, high-quality health system that provides cost-effective, direct, and far more seamless care than patients are receiving today.

Recommended Resources

Data Sources